HBD Bond Market

Bonding is a concept that gets talked about a lot by @taskmaster4450. Personally, I have casually dismissed the idea a few times because it lacks the one fundamental requirement of any loan: two parties that mutually benefit.

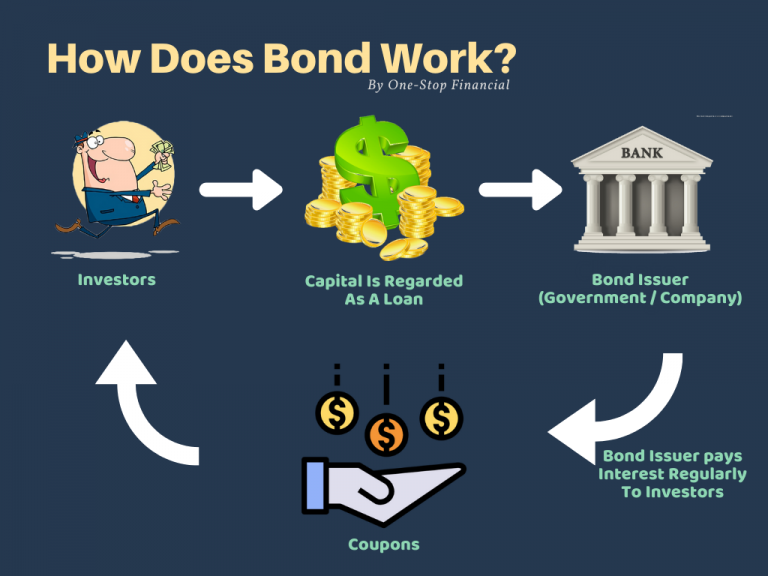

Every loan has two sides: a lender and a borrower.

The borrower always has an incentive to get a loan. Liquidity matters. If we can get money today we can leverage it in various ways to grow that loan into more value than we have to pay back later. By the time we pay back the loan we hope that more value was created than lost. That's the theory anyway.

Even in the case of a car loan, where the value of the vehicle depreciates 10% a year, we still assume that the car is ultimately worth more than the price because we need it to get more money (even if it's just commuting to a 9-to-5 job). In this case it is not the value of the car that maters but the value of convenient transportation & logistics the car provides over its lifespan. Some people use a car that they own to go pretty much everywhere. This provides an extremely versatile asset that can be leveraged in dozens of scenarios.

It is even more obvious why one might need a business loan or a house loan. The vast majority of the time it is not an option to buy these big ticket items upfront. It will be interesting to see if cryptocurrency can change this. Is it possible that within an abundance economy of exponential growth that citizens will no longer need loans because they already have all the money they need to do these things? It's quite possible; with DEFI protocols like MAKERDAO we see it is already possible to give ourselves loans permissionlessly with overcollateralized assets. That's powerful.

But what about the lender?

The borrower always has a reason to borrow money. This is especially true considering the guaranteed declining value of fiat currency. It's a little different when we borrow Bitcoin to short it, but that's a new story entirely.

As we all know, a lender demands interest on the loan to make the deal worth it for them on their side. Without this yield, their would be no reason for the loan to occur. Both sides need to be getting something out of the deal, otherwise the deal will not happen.

This is why I poo-poo the idea of HBD/crypto bonding.

Because the lenders are the users on Hive that deposit HBD into the contract, and the borrower is the platform itself. So sell me, why does the platform itself need to borrow money? Long answer short: it does not. Hive prints money out of thin air, why would it need to borrow more on top of that? Make it make sense!

And so this idea of bonding within the cryptosphere becomes an unsustainable pyramid scheme just like fractional-reserve banking. The borrower (Hive) can not leverage the money borrowed into more value than was borrowed. Thus the entire scheme just becomes a horrific short-sighted pump and dump where we pump the price today only to have it crash into the mountain once the bill comes due and we owe back more debt than was issued (for no other reason than greedy and unsustainable number-go-up mentality).

When a government issues a bond, they are taking a loan directly from the citizens. Do we think the government just sits on that money and does nothing with it? No, of course not. The government issued the bond because it wants to spend that money now and pay it back later, just like any other entity that borrows money. Crypto platforms aren't advanced enough to do this yet, and so I have, on multiple occasions, casually dismissed this idea of bonding on the blockchain.

The problem with this assumption is... I'm kind of an idiot!

Like, I hardly know anything about bonds, and people like @taskmaster4450 know a metric shitton about financial instruments such as this... so for me to casually dismiss the entire idea based on a single caveat is extremely presumptuous and downright lazy and bad practice on my part.

So rather than be that guy and just assume I know everything without doing any research, I decided to take a rudimentary Google tour of bonds and how it works. The results of that short journey were... enlightening.

Am I conflating?

One of my big arguments against rewarding 20% APR to Hive users for locking HBD into the savings accounts is that we are rewarding users for taking liquidity away from the network. We shouldn't want HBD to get time-locked away in a smart contract. Again, this is perhaps good for pumping Hive in the short term (or if done well: stabilizing the price of Hive with dynamic changes to yield) but really bad for increasing liquidity on a rather already illiquid network. This is why I often make the claim that yields like this should be applied to yield farming an AMM LP on the internal market, as that would actually create exponentially growing liquidity between Hive and HBD rather than locking up assets and not using them for the greater good.

Am I conflating?

The problem is that I use the same argument against Hive bonds. Bonds are a bad idea because it's the same concept: we would be rewarding users for time-locking stake and creating more illiquidity. However, anyone that knows anything about the bond market will realize instantly that this logic is completely wrong. The bond market is one of the most liquid derivative markets on the entire planet.

So then I began to realize rather recently that with a bond market: you get the best of both worlds. You get to have your cake and eat it too. We can lock up HBD while still providing exponentially increasing liquidity to the HBD market. This is the magic of derivative assets.

The big hurdle in understanding for me is the raw nature of a bond. A bond is a loan. Within the context of crypto, a bond is an NFT. No two NFTs are alike. NFTs are not fungible, and thus loans are not fungible, and thus bonds are not fungible. If I buy a bond today and get paid back in ten years, this is not the same as a bond that was taken out 3 years ago and gets paid out in 7 years. Both are 10-year bonds, but they are not the same because the payout date is different. How then... can the bond market possibly be the most liquid market in the world?

The largest and most liquid market in the world is the forex market, where foreign currencies are traded. It is estimated that the daily trading volume in the currency market is over $5 trillion, which is dominated by the U.S. dollar.

$5T lol wtf?

Okay so not THE most liquid market but a very big one. How is it possible that the bond market is so liquid when it is composed entirely of NFTs? It just didn't make sense. This required another Google search.

On issue day, the Treasury delivers securities to bidders who were successfully awarded securities. In exchange, Treasury charges the accounts of those bidders for payment of the securities. The final price, discount rate, and yield is released to the public within two hours of the auction.

Oh....

Okay so the Treasury runs this crazy bond market auction house, where people buy and sell the debt on the open market. Now it all makes a bit more sense. Non-fungible loans are efficiently turned into fungible assets using this clever trick of selling them at auction. I bet I could easily write an entire post just on how this auction house works, but that's well beyond the scope of this post (and also I have no idea how it works; I'd have to do more research). The point is... everything makes sense now; it's all starting to come together.

If HBD had a bond market:

- Bonds would be NFTs.

- These NFTs would generate static yield.

- This NFT market would have an auction house to create virtual fungibility, exponentially increasing liquidity.

- The auction house materializes variable yield.

- Hive is lender.

- Hive is the borrower.

The auction house materializes variable yield.

Another interesting outcome of the derivative bond market: being able to sell a bond before it matures means the interest rates can change. For example, if I am five years into a ten year bond and I don't want to wait another five years to get my money back, I can just dump it on the auction house no problem. However, what happens when a bunch of people all dump their bonds at the same time? Basic logic dictates that value of the bonds will drop and we will get less money in return for selling it.

Something I had never considered until now:

When the bond market is bad and there is less demand to hold the debt, interest rates will go up. Kind of a weird counter-intuitive outcome, but it's true because if people are willing to sell a bond for less than its face value the virtual yield will appear to go up (when in reality the buyer just got a good deal in real time). However, it isn't really viable to show that the buyer got a good deal on the spot-price of a bond, so rather the interest rate is manipulated to reflect the good trade. That probably doesn't make a whole lot of sense because it barely makes sense to me. Perhaps I have more research to do.

It's also important to note that all bonds have a floor price as determined by the government. If the debt on a bond reaches this floor price: new bonds will be issued rather than being traded on the derivative market auction house. For example, you wouldn't buy a bond on the auction house that provided 4% yield if you could just buy one directly from the government at 5% yield. The government can control the floor but they are completely powerless to control how high interest rates go due to selling.

And now, all of a sudden a lot of the things that @taskmaster4450 has said in the past make a lot more sense to me.

People own the debt, and thus people set the interest rate. This is especially true during a recession, as the demand for liquidity grows and people become more and more willing to sell their bond at a perceived loss in order to get cash on demand today. This is how the yield curve can become inverted, as those who bought short term bonds dump them early and spike the rates.

Imagine if the housing market or stock market collapses. All of a sudden anyone can buy property or stock at a 50% discount. How many people holding bonds would see that as a massive opportunity to rotate their value out of debt and into the riskier markets? Something to think about.

Inflation also messes with bond yields. If the perceived value of USD is going down very quickly, a bond that pays out 5% interest is not very attractive. What's the point of buying a bond if the yield on it is less than fiat devaluation? Someone would only take this deal in the riskiest of scenarios where there is no other safe place to put the money.

If something like Bitcoin becomes safer than bonds... the entire bond market would implode because there is no way legacy bonds would be able to compete with superior crypto yields. Be on the lookout for more claims that crypto is a threat to the economy. It isn't now... but it's funny because they seem to know it will be (or maybe it's just all propaganda and lies). In reality, it is not crypto that threatens the legacy system, but the legacy system that threatens itself. Welcome to the pyramid scheme that is legacy finance.

Hive is lender; Hive is the borrower.

So back to the original point of contention: "We shouldn't do bonds because Hive can't leverage the money into more value." Even this is not true when looked at more closely. HBD being locked up in a bond contract intrinsically increases demand for our debt. Increasing our demand for debt means more HBD must be printed. The only way to print HBD on demand is to destroy Hive. Destroyed Hive increases the spot-price by lowering supply.

Within this context it becomes clear that in terms of HBD bonds, the HBD holders (bond holders) are the lenders, and Hive holders are the borrowers. Everyone that holds Hive would then have the ability to sell it at a higher price if they desired. To make the claim that we cannot collectively leverage this debt into more value is flat out incorrect.

The reason I did not initially think about it in this way is because decentralization is often confusing and contrary to all other things in life. In the case of government bonds, the government is the centralized borrower. It much stranger to think about what things would be like if the borrower was not only decentralized, but actually unilaterally controlled their own currency. As we all know, the Federal Reserve is not 'federal' at all, but rather a private bank. This means that many of the variables involved with this kind of DEFI are completely backwards compared to legacy systems. In many cases the brain must be completely rewired to even begin theory-crafting these ideas.

Leveraging the derivative market into HBD liquidity.

So not only can we lock up a massive amount of HBD for x length of time, but also the NFTs we create from those locked contracts could be bought and sold on the open market as a derivative asset. Imagine it: HBD paired to... HBD... lol.

Talk about stable coin.

The HBD/HBD pool.

1 HBD = 1 HBD.

Of course one side of that equation would be NFTs that represent bonds that pay out HBD later, but you get the idea. Technology like this could create exponential demand for our debt while simultaneously creating exponentially large liquidity pools for HBD, which again feeds into creating even more demand for our debt.

It's also highly significant that bonds have been around since 1935.

On February 1, 1935, President Franklin D. Roosevelt signed legislation that allowed the U.S. Department of the Treasury to sell a new type of security, the U.S. Savings Bond. One month later, the first Series A Savings Bond was issued.

Why is this important?

Because the way bonds work reflects the fact that the Internet did not exist when they were initially created. We can leverage this failure and lack of evolution into our own product. For example: it is not possible to buy a bond that is permanently locked.

Long Bonds Explained

For the U.S. Treasury market, this includes the 30-year Treasury which has the longest maturity of all offerings. Corporate bonds, however, can issue maturities in different variations. Corporate bonds may offer maturities of 15, 20, or 25 years.

Why can't bonds be permanently locked? Because the interest payouts are rolled into the principal and not unlocked until maturation. We don't have to follow that rule; we could easily create bonds that are permanently locked and simply dish out interest payments that are unlocked. Something like this was not really possible in 1935, so it wasn't even considered. We aren't bound by these limitations and can experiment with these things in whatever way we want. Too-big-to-fail systems that have been established for generations are not agile enough to evolve or test new solutions.

Possible implementations

We should NEVER expect that something like this would be coded directly into the base-layer on Hive with a hardfork. Even in the best case scenario, something like this needs to be tested for years on the second layer and have massive success before it would be ready for layer-one adoption.

Two possible options:

- Funded by corporation/DAO

- Funded by Decentralized Hive Fund @hive.fund

In the case of corporate funding a corporation on Hive would build the bond NFTs and the auction house and issue the loans in a centralized way via their own platform. The corporation would then have to leverage the loans they took into building other projects on Hive that generate revenue/value.

In the case of DHF funding we'd simply subsidize the yields using the community pot. In essence, the yield was printed out of thin air. Again, this is a centralized solution controlled by the dev that builds it, but there are possible decentralized vectors that could be pursued like multi-sig on the bond wallet to make sure it doesn't get hacked.

Then again, it would be very difficult to hack something like this because the vast majority of HBD would be locked for 3 days in the savings account. The required amount of unlocked liquidity is a tiny amount equal to matured bond payouts (meaning unlocked liquidity can be zero while there are no bond payouts pending). In fact, unlocked liquidity could be zero 99.9%+ of the time because the payouts could be perfectly timed with a bot, ensuring that at most only one payout was in the wallet at one time (or even fractions of a payout transferred incrementally).

Network effect and interoperability

Another point of note: anyone who builds this protocol could easily recycle the code for other projects. If bonds are NFTs and virtually liquid/fungible through an auction house protocol, that auction house can then be leveraged to sell other types of NFTs (and perhaps even make those other NFTs fungible as well on a certain level, such as floor price). Again, this is a testament to open-source technology and our ability to create modular applications. Obviously something like the legacy bond market can not be recycled into a new project like crypto can do on a whim.

The opposite is also true. It might not be that hard to leverage a currently existing NFT auction house into one that can service a bond market. In fact, this is the most likely scenario: leveraging code that already exists into second-layer bond NFTs. Fun story: my witness clique already has such a product. It's called NFTMart and it's primarily run by @cadawg and @rishi556.

https://nftm.art/

I guess now is an appropriate time to shill our witness node @hextech.

Vote for @hextech!

Or not! Your choice.

@cadawg has a witness running as well.

Circling back to interoperability, if we create a platform for bonding on Hive, it may not be that difficult to leverage that protocol into other networks. The frontend of this protocol would be a big chunk of the code, and switching backends might not be that difficult. Unfortunately, in this case, the DHF is no longer a viable solution for yield, and it would be up to corporate bonding to leverage the debt into value for all parties concerned.

For example, a corporation minting bonds on Hive could suddenly find themselves printing very similar bonds on the Ethereum mainnet, or even virtually on the Bitcoin network using centralized custodianship. Is such a thing legal? I'm sure the regulations for issuing bonds is not a simple thing, but it's still worth mentioning.

A big problem with this would be the fact that BTC and ETH are not stable coins, thus borrowing BTC or ETH is very akin to shorting the market, which could be very risky, but could also be used as a hedge when combined with the corporation's long positions. Definitely makes more sense in terms of a stable coin like DAI, USDC, USDT, etc, assuming we want more traditional bonding.

@khaleelkazi & LEO/CUB bonds.

LEOfinance is working on an interesting version of bonding as well. However, the way in which it increases demand for debt is a little different. In this case the bonds will be issued to outsource bad debt rather than overleveraging good debt. The plan is to allow polycub users to lock their pCUB into a smart contract that can pull stable-coins out of the communal vault. However, should the pCUB collateral fail, the communal vault will then own the bad debt in the form of pCUB collateral. This has proven to be a problem to other loan networks like MAKERDAO, and can end up in a black-swan situation where liquidations create a death-spiral cascade of compounded liquidations.

The pCUB bonding protocol will outsource this bad debt in the form of bonds that allow users to buy the debt for a good yield over time rather than having to immediately dump all the tokens onto the market. It's an interesting concept and I patiently await this development to materialize in the sooniverse.

Conclusion (TL:DR)

This monstrosity of a post has reached over 3000 words.

Time to kill it.

After careful consideration, a bond market for crypto can be leveraged into a win/win scenario where the original token is locked for years (or permanently) and the derivative assets are then utilized as NFTs to create massive liquidity pools between the collateral and the derivative. The HBD/BOND pairing would be quite valuable indeed. Maybe even enough to get the world to stop ignoring us :D. Dare to dream.

Posted Using LeoFinance Beta

Cool perspective on Hive bonds, I still don't understand how this concept can help this ecosystem and its effects.

U can do this with honeycomb technology side-chain already (DLUX alike). And its actually very easy. So, really interesting 🤔 after reading all this. I am not myself a fan of bonds, but I confess the idea of trying like this would be something cool to try.

Give me a shout if u find anyone going forward. I will run a node for consensus easy.

I am working on developing a complete financial framework that expands upon this idea. Some of what is spelled out here is being outlined.

Certainly think about Honeycomb technology about the build out of this.

Posted Using LeoFinance Beta

👀 - ping me wen (if I forget and you recall).

Bonds have a yield. In other words, they pay a certain amount.

For example, a $10K 10-Yr might pay $200. That is what the bond pays based upon the par value. It pays this whether the bond is sold for more than $10K or less.

Going to an extreme, if the bond is sold for 20K, it still pays $200 annually. This means the yield moved from 2% to 1%. The opposite is true. If the bond sells for $5K then the yield moves to 4% since it still pays $200.

A 10-Yr last year paid $175 a year on $10K. Now it is $375? Why would anyone pay $10K for $175, when they can get $375 on new bonds. They wont. That is why the price has to go down, to get the yield near the 3.75%.

Posted Using LeoFinance Beta

Treasuries are so corrupt given central bank crony buying and what not. Not to mention anyone loses money buying here with inflation rate being higher. I wouldn’t be shocked if the Fed has a shadow beldncr sheet and I’d still buying more then claimed during this “unwinding” that’s hardly started of Balsnce sheet. It’s a shame it’s so corrupt, but legit bond market not corrupted would be interesting indeed.

Btw really love these conversations 👍

I really enjoy it. I should of been listening from way back but better late then never! I’m sending Boosts every episode 🙌

Anyone reading this who hasn’t definitely look up this podcast on ur podcast app ⬇️

Or on fountain here ⬇️

https://fountain.fm/episode/10695664108

As for the auction, that is done through the 24 primary dealers (banks) that are authorized to buy bonds through the Fed auctions. These can be bought for in-house accounts (the banks warehousing) or on behalf of clients (pension and hedge funds, insurance companies, etc...).

Different bills or bonds are put up each week (according to the schedule). The dealers big on them, pushing rates up or down. The Treasury has a price that it sets based upon a 365 day yield curve each asset it runs.

Of late, TBills have gone for yields much lower than the reverse repo "floor" (meaning they paid up for the bonds). Why would bankers accept 40%-50% less yield than they can get in the reverse repo market on that security?

This is the other point of the entire discussion: they need the collateral.

Hive bonds are a leg into the collateral game. It is, in my view, a pristine asset, since the HBD is locked in a time vault, all aspects of the bond creation and transaction is transparent, the stream of payments along maturity are clearly defined, and the blockchain is not going to default since the interest payments and payout at maturity is written into the code.

No 3rd party countrisk.

Posted Using LeoFinance Beta

Another thing to keep in mind:

When Treasury bonds are sold, the USD goes into the TGA at the Fed. From there, the Treasury sends out payments in accordance with government spending. In other words, the USD is still in circulation. Already circulating USD is used to buy the bonds and the government sends the money out which is then used by individuals and companies. No new USD is created nor destroyed. It is circulating as it was before.

With Hive bonds, it isnt exactly the same. The HBD is locked up in a time vault. Hence the NFT (to use your term) is nothing more than a transforming of the HBD that is backing it. There is no "borrowing" in the sense since the HBD is not used while the bond is in effect. Only at maturity will the HBD be released and back into circulation.

Hence I look it as a matter of not creating more as much as simply transforming the state of the money. It is akin to water and ice. HBD is water that is frozen (put in time vault) and we end up with ice (bond/nft).

We are just adding liquidity on the second layer to HBD that is locked up at the base layer. The best part is the bond can then be collateralized in other applications.

Posted Using LeoFinance Beta

And yes we use HBD (or some derivative of it) on the exchange that is trading the bonds. This is how we create our own system for HBD use. So you are correct, HBD is used to create the bonds while more HBD is swapped for the bonds, and the bonds are really nothing more than future HBD.

Posted Using LeoFinance Beta

This post has been manually curated by @bhattg from Indiaunited community. Join us on our Discord Server.

Do you know that you can earn a passive income by delegating your Leo power to @india-leo account? We share 100 % of the curation rewards with the delegators.

Please contribute to the community by upvoting this comment and posts made by @indiaunited.

I stopped reading half way through it, just a few paragraphs after

The big issue is when hive goes up, that hbd won't be shit. So hbd bets directly against hive, when hive is down, that hbd is a lot of hive, with the APR at 20%, it will be a joke to power up.

A pyramid scheme pays old investors with money from new investors, the important characteristic being that VALUE pours in, and is syphoned away by the schemers. In our world, nobody is really scheming, its all on the up and up, what backs a bond? Government, or as the fed says, the future power to tax, and the Belief in the Currency that you can redeem it in, or Full Faith and Credit of American People.

My faith in the credit of the American people is reflected in my bond portfolio, which doesn't exist. I happen to know some American people and I wouldn't lend them a boomerang. It would never come back to me.

ouf, I'll have to re-read that

I reckon your readers know this, at least the vast majority of them, but not all of 'us', meaning the general public. I think most of the general public think dollars are not debts to a private bank, but somehow tax receipts printed by the actual federal government.

Not your main point, but all I'm remotely competent to address, other than to point out that financialization can be really, really bad for real things, like moms, food, and forthright speech. It's excellent you have undertaken to learn how bonds work in practice, because not knowing how things work rarely ends well.

Thanks!

Prison

“ Okay so the Treasury runs this crazy bond market auction house, where people buy and sell the debt on the open market”

Well generally it’s where one’s own central bank buys a large portion of its own nations bonds like a Banana Republic… as we see how in England.

But obviously overall point you made makes sense. I still have concerns but you did a good breaking this down indeed!